Reporting Through Ambiguity: California’s CCDAA and the Future of Sustainability Reporting

By Christian Bakken and Josh Lowell

A Landmark Ruling

When California Governor Gavin Newsom signed the Climate Corporate Data Accountability Act (CCDAA) in 2023, the implications were clear: California was enacting the most ambitious corporate climate disclosure requirements in the United States, with two climate disclosure mandates:

A Complicated Rollout

While the overarching disclosure may have been signed into law, CCDAA's implementation has been marked by litigation, regulatory delays, and shifting requirements, leaving those subject to disclosure in a fog of uncertainty. The most recent updates were just released on June 24th, 2026, delaying the reporting deadline by three months to align with forthcoming changes. Here is where we stand:

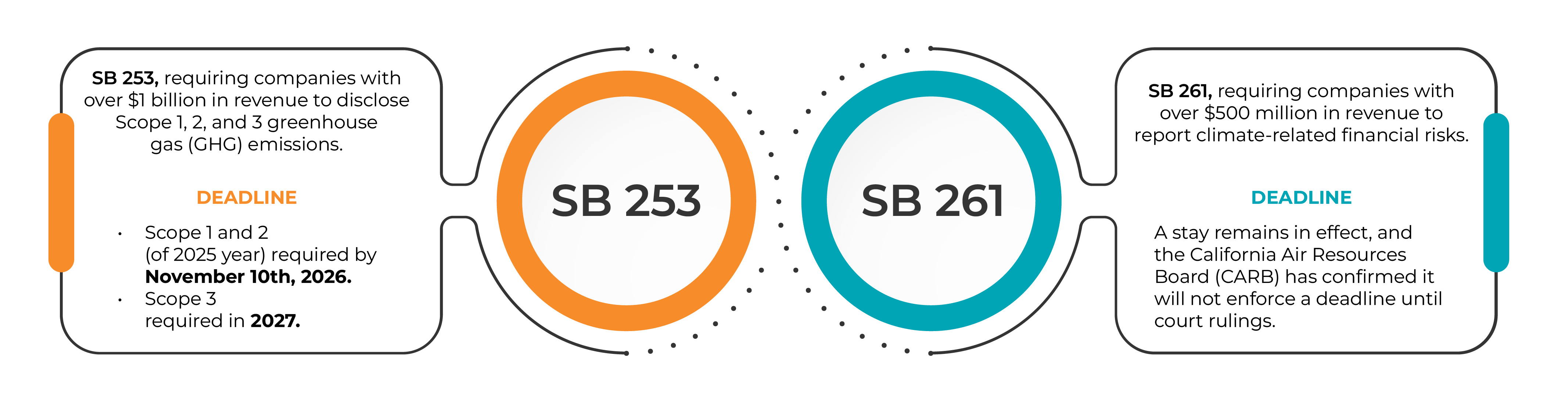

SB 253

Work is still being done to finalize a mandatory reporting template. The draft template published in October 2025 is available, but voluntary; CARB has communicated that companies can submit reports in any format that includes their Scope 1 and 2 emissions. This will likely lead to inconsistent reporting in year one, leaving companies to individually interpret the requirements on their own, and investors to review inconsistent disclosures. CARB deferred the first-year assurance requirement, and companies submitting in 2026 will not need third-party verification. This is a significant departure from the statute's original design. On the horizon, additional legal challenges are anticipated, both for scope 1 and 2 and for the Scope 3 emissions reporting disclosure.

SB 261

After the laws were enacted, the U.S. Chamber of Commerce and other business groups filed a legal challenge, arguing the disclosure mandates constitute ‘compelled speech’ under the First Amendment. On November 18, 2025, the Ninth Circuit Court of Appeals granted an injunction halting enforcement of SB 261 pending appeal, just weeks before its January 1, 2026 compliance deadline.

Why Preparation Still Matters

Despite the ambiguity, delaying compliance preparations due to current uncertainty is a strategic miscalculation. Companies should be taking this opportunity to strengthen data management and reduce operational risk now.

Here is why:

1. Mandatory Sustainability Disclosures Is the Global Trajectory

The Securities and Exchange Commission (SEC) may have stepped back, but the rest of the world has not. The European Union (EU)'s Corporate Sustainability Reporting Directive (CSRD) is already requiring thousands of companies to disclose standardized sustainability information. As of January 2026, more than 21 jurisdictions have adopted the International Sustainability Standards Board (ISSB)'s International Financial Reporting Standards (IFRS) S1 and S2 standards, covering approximately 60% of global gross domestic product (GDP), with over 40 additional jurisdictions in active adoption processes.

China's Ministry of Finance issued a climate disclosure standard based on IFRS S2 in December 2025, signaling that the world's second-largest economy is building toward a nationwide sustainability reporting framework by 2030. Japan, Australia, Singapore, Hong Kong, Brazil, and the United Kingdom are all in varying stages of ISSB-aligned reporting.

Within the United States, the trend is equally clear. The New York State Senate passed its own Climate Corporate Data Accountability Act (S9072A) on February 10, 2026 by a 40–22 vote, mirroring California's SB 253 and requiring Scope 1 and 2 disclosures starting in 2028, with Scope 3 in 2029. We expect other states to introduce their own disclosure requirements in the coming years.

2. Reporting Creates Business Value

Sustainability reporting is not a compliance checkbox, but a lens into a company's operational risks and opportunities. According to PwC's 2025 Global Sustainability Reporting Survey, 80% of companies that report under CSRD or ISSB expect to derive moderate or significant business value from the sustainability data they collect. Investor demand is a major driver- 87% of surveyed U.S. companies indicated they will produce ISSB-aligned public reporting, and external pressure to provide sustainability data increased for 42% of U.S. firms in the past year.

3. Sustainability Performance Drives Capital Allocation

Investors are increasingly embedding sustainability criteria into how they deploy capital. Sustainability performance now influences not just whether companies are eligible for inclusion in certain funds and indices, but how capital is distributed among peers through portfolio concentration, position, sizing, and allocation strategies.

EY's Global Institutional Investor Survey from 2023 reinforces the point: 99% of investors surveyed use sustainability disclosures in their investment decision-making, with 74% employing a rigorous, structured approach, up dramatically from 32% in 2018. Companies with stronger sustainability governance, strategy, and disclosure quality are more likely to attract favorable positioning within sustainability-focused portfolios.

4. Weak Reporting Invites Legal and Reputational Risk

Scrutiny of corporate sustainability claims has been on the rise, with greenwashing cases nearly doubling since 2020, reaching an estimated 2,700 globally in 2025, and the examples are still mounting.

In October 2025, the Paris Judicial Court handed down a historic ruling against TotalEnergies. The court found that TotalEnergies' claims of being a "major player in the energy transition" with an "ambition to achieve carbon neutrality by 2050" were misleading given its continued expansion of fossil fuel production. The company was ordered to remove the language from its website within 30 days and chose not to appeal. Meanwhile, Apple faced a class-action lawsuit over "carbon neutral" marketing for its Apple Watch, with plaintiffs alleging that the offset projects backing those claims failed to deliver real reductions. While the U.S. case was dismissed in February 2026, a German court separately barred Apple from advertising the watch as carbon neutral, finding its offset methodology insufficient.

The Bottom Line

Despite the short-term ambiguity, sustainability reporting is already a fixture for global business. The trajectory is set, decisively, toward mandatory, standardized climate disclosure. Investors are expecting it. Regulators are building it. Companies that invest in robust, credible reporting now will be better positioned than those that scramble to catch up later. RE Tech has long supported clients in preparing for regulatory implementation, including 100+ framework-aligned reports, analysis of the carbon footprints of 20,000+ buildings, risk discovery and mitigation that helped organizations avoid over $3.2B in fines, and rigorous data management. Reach out today to enhance your journey towards compliance.

We are hiring!

We are looking for creative and energetic professionals that are passionate about sustainability, real estate, using data and analytics to drive results, and making a difference. Come join our team.